Despite remaining one of the world’s poorest nations and operating in one of Africa’s most complex environments, the Democratic Republic of the Congo (DRC) is on track to become the continent’s eighth-largest economy in 2026.

- +Rising DRC: How Congo is climbing into Africa’s largest 10 economies

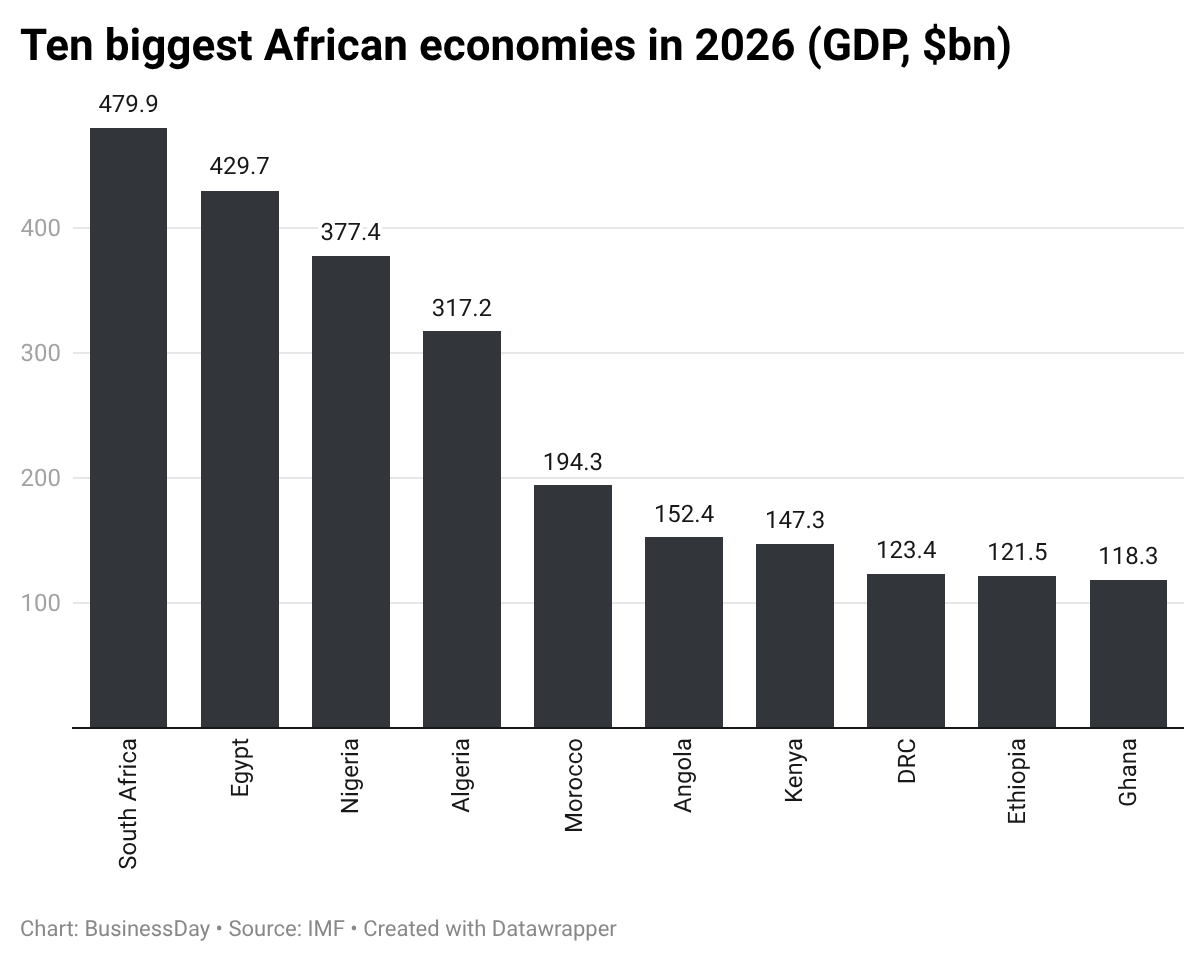

BusinessDay analysis of GDP data across 53 African countries, based on estimates from the International Monetary Fund (IMF), shows the DRC climbing from 11th place last year, overtaking Ghana in the process.

BusinessDay analysis of GDP data across 53 African countries, based on estimates from the International Monetary Fund (IMF), shows the DRC climbing from 11th place last year, overtaking Ghana in the process.

The IMF projects the Central African economy will reach $123 billion, slightly ahead of Ghana’s estimated $118.3 billion. South Africa is expected to retain its lead at $479.9 billion, followed by Egypt ($429.7 billion), Nigeria ($377.4 billion), Algeria ($317.2 billion), and Morocco ($194.3 billion).

Across sub-Saharan Africa, the DRC is also set to become the fifth-largest economy, overtaking Ethiopia.

Congo’s rise is underpinned by a mining boom and renewed investor interest in its vast reserves of critical minerals.

The country holds some of the world’s richest deposits of copper, cobalt, and lithium—resources central to electric vehicles and the global energy transition. This has drawn multinational mining and logistics firms requiring trade finance, treasury, and corporate banking services.

Momentum has also been supported by improved market conditions and a temporary easing of geopolitical tensions, enabling the country to raise $1.25 billion through its debut Eurobond.

Currency stability has further reinforced the outlook. The Congolese franc has appreciated by more than 25 percent against the dollar over the past year, contrasting sharply with Ethiopia’s birr, which weakened following currency liberalisation in 2024.

According to the World Bank, the Congolese franc and the Zambian kwacha were among the region’s strongest-performing currencies, appreciating by 28 percent and 26 percent year-on-year, respectively, by end-2025. “The appreciation of the Congolese franc was underpinned by higher foreign exchange reserves, supported in turn by stronger global demand for copper.”

The Bank added that lower inflation, targeted foreign exchange interventions, and liquidity management measures by the Central Bank of Congo also played a key role.

The DRC is increasingly attracting interest from global players seeking to secure critical mineral supply chains.

United States-backed ventures such as KoBold Metals, alongside projects led by China’s Zijin Mining Group, are expanding their footprint as demand for battery materials accelerates.

A recent report from the African Economy noted that a US State Department official described investor interest as “significant,” although discussions remain at an early stage and are tied to broader peace efforts in eastern Congo.

Earlier this year, the Congolese government submitted a list of strategic mining assets to Washington, including projects in manganese, copper, cobalt, gold, and lithium. The initiative forms part of a broader push to attract Western investment and reduce reliance on Chinese supply chains.

A key asset is the Rubaya coltan mine—one of the world’s richest sources of tantalum—but its location in a conflict-affected region controlled by the M23 rebel group continues to complicate investment prospects.

Despite its improving economic ranking, the DRC’s growth is projected at 5.9 percent—below Ethiopia’s expected 9.2 percent expansion. Sub-Saharan Africa is forecast to grow by 4.3 percent in 2026.

The country remains among the 10 poorest globally, with over 70 percent of its estimated 109 million people living in poverty. Financial inclusion is also low, with fewer than 39 percent of adults holding a formal bank account, according to the World Bank.

Yet for banks, this gap represents opportunity.

Regional lenders are expanding aggressively into the DRC, drawn by its scale, resource wealth, and underbanked population.

From Nigeria’s Access Holdings and FirstHoldCo to Togo’s Ecobank, Kenya’s Equity Group and KCB, and Tanzania’s CRDB Bank, institutions are increasing their presence in a market once considered too risky.

Equity Group entered in 2020 through the acquisition of Banque Commerciale du Congo (BCDC), now Equity BCDC. KCB followed in 2022 with an 85 percent stake in Trust Merchant Bank.

Nigeria’s Access Bank has operated in the country since 2008, while FirstHoldCo’s presence dates back to 1994. Ecobank entered in 2008, with United Bank for Africa following in 2011.

Another Nigerian bank, Fidelity is the latest entrant, with plans to launch operations focused on digital inclusion. Once operational, it will become the 16th active bank and the fourth Nigerian lender in the country.

Despite this expansion, the sector remains small relative to the economy, with just 18 licensed commercial banks—mostly foreign subsidiaries.

According to the Making Finance Work for Africa Partnership (MFW4A), a handful of large institutions dominate the market, led by Rawbank, which recently climbed to 62nd position in Africa’s top 100 banks ranking with Tier 1 capital of $421 million.

The mining sector is a major driver of corporate banking activity. Multinational mining firms require foreign exchange services, trade finance, and project financing—creating steady revenue streams for banks.

The African Development Bank (AfDB) estimates that trade-related activities now generate nearly 15 percent of total bank income across the continent.

Mining also stimulates small and medium-sized enterprises within supply chains, further boosting demand for credit.

The World Bank estimates the DRC economy grew 6.5 percent in 2024, driven largely by a 12.8 percent expansion in extractive industries.

The DRC’s accession to the East African Community (EAC) in 2022 has enhanced its economic appeal.

As the bloc’s seventh member, the country benefits from expanded market access, policy alignment, and improved cross-border banking regulations.

Former Kenyan President Uhuru Kenyatta noted that the DRC’s inclusion expanded the bloc’s population to 300 million and its combined GDP to $250 billion.

For banks, the EAC framework supports cross-border payments, remittances, and digital banking integration.

Digital finance is also closing the inclusion gap with fewer than 200 physical bank branches nationwide, digital finance is rapidly transforming access.

Telecom operators Vodacom and Airtel have built extensive mobile money ecosystems, enabling millions to transact without traditional banking infrastructure. Banks are partnering with telecoms to onboard customers digitally, leveraging agent networks and biometric verification.

This shift is helping close the inclusion gap, with account ownership rising from 17 percent in 2014 to 39 percent in 2024, according to the World Bank.

Development institutions are playing a key role in de-risking the market.